P2P Payment Apps in the U.S.: Adoption Rates by Age Group (2018-2025)

Peer-to-peer payment apps have fundamentally reshaped how Americans transfer money, with 76% of U.S. adults now having used at least one platform like PayPal, Venmo, Zelle, or Cash App [1]. For merchants, understanding these adoption patterns is not just interesting trivia – it directly informs which payment methods to accept and how to reach different customer segments effectively.

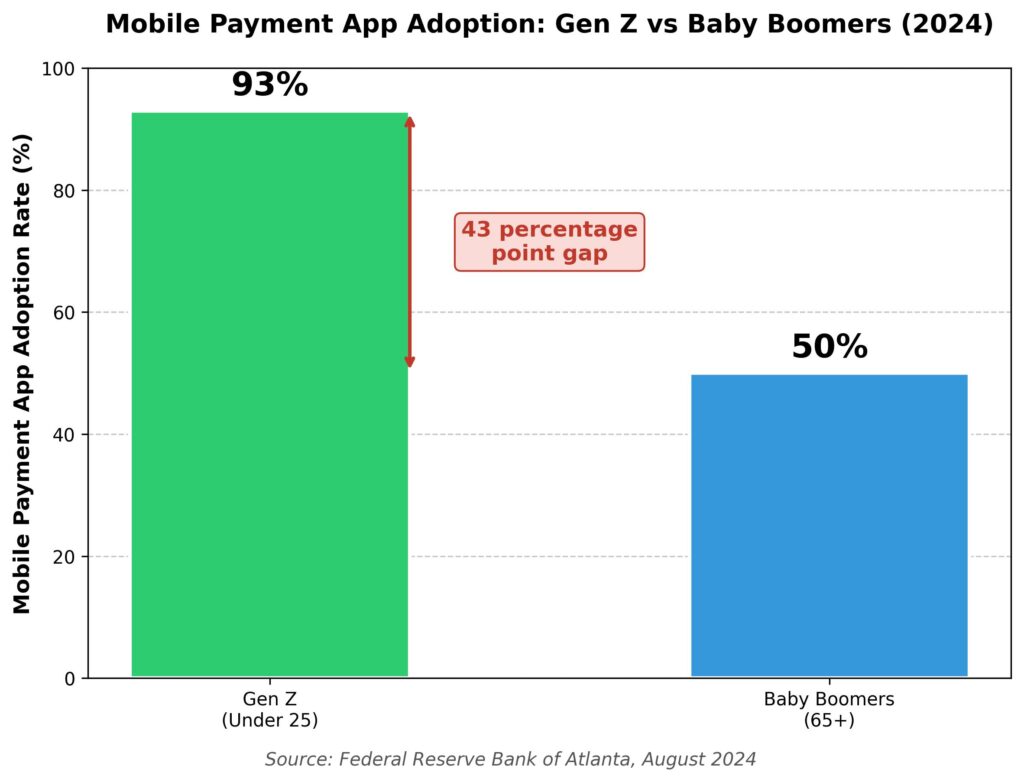

The generational divide in P2P adoption is striking: 93% of Gen Z consumers (under age 25) have adopted mobile payment apps compared to just 50% of baby boomers and older adults (65+) [2]. This 43 percentage point gap represents both a challenge and an opportunity for merchants seeking to serve customers across age groups.

This analysis examines P2P payment adoption data from authoritative sources including the Pew Research Center and the Federal Reserve Bank of Atlanta. The data reveals clear patterns that every merchant should understand when making decisions about payment infrastructure.

Overall P2P Platform Adoption

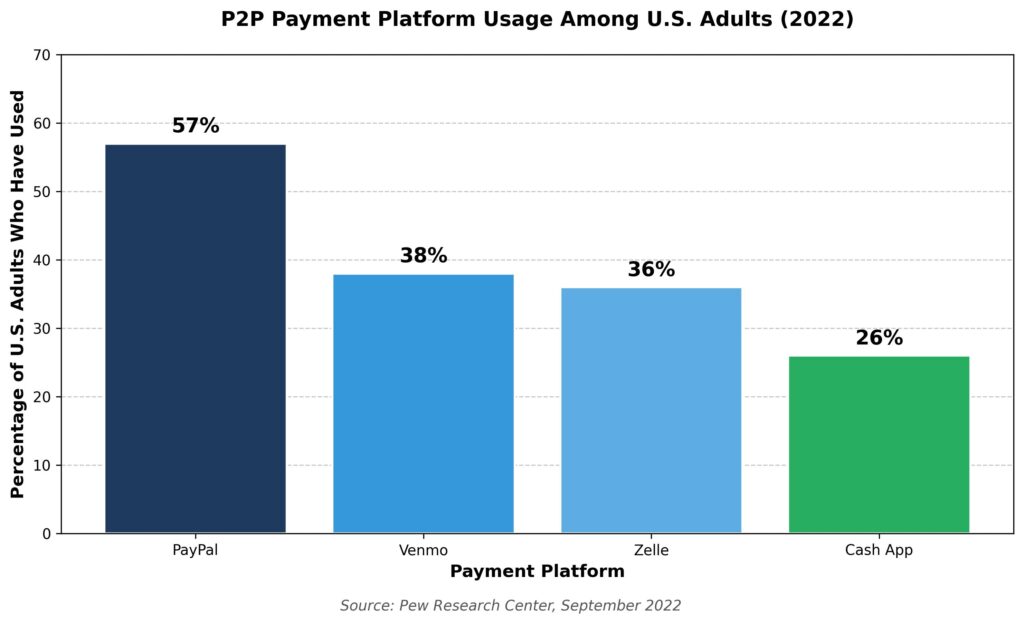

PayPal leads all P2P platforms with 57% of U.S. adults reporting they have used the service [1]. Venmo follows at 38%, Zelle at 36%, and Cash App at 26%. These figures represent ever-used rates rather than active monthly users, but they indicate the broad familiarity Americans have with these platforms.

For merchants, PayPal’s dominance makes it a safe baseline choice for online payment acceptance. However, the relatively close adoption rates of Venmo and Zelle suggest that offering multiple P2P options can capture customers who prefer specific platforms.

The Age Gap in P2P Adoption

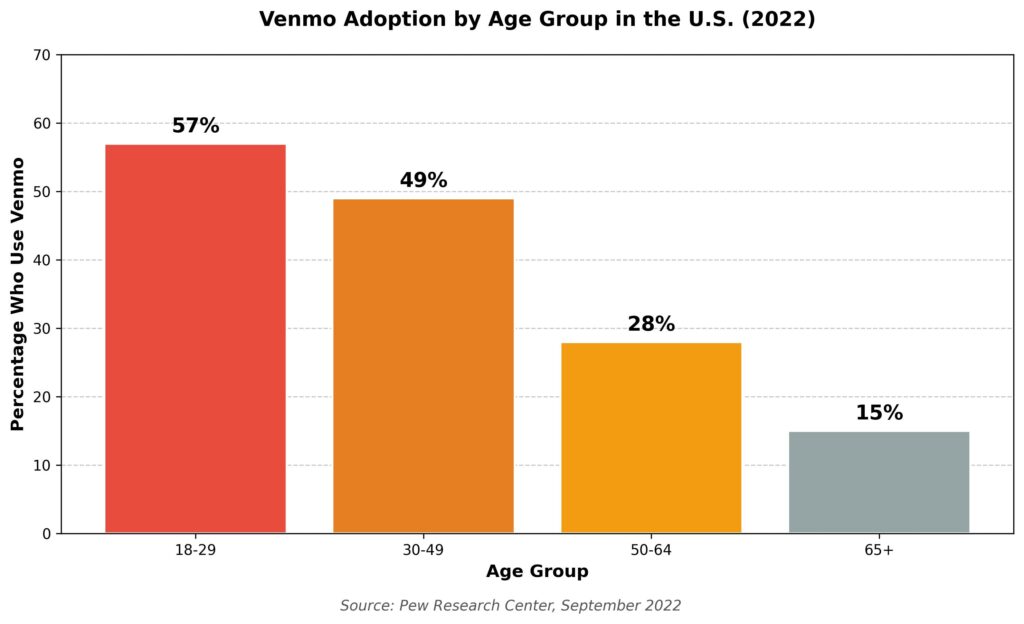

Age is the strongest predictor of P2P payment adoption. According to Pew Research, the age gap is most pronounced for Venmo: 57% of adults aged 18-29 use the platform, compared with 49% of those 30-49, 28% of those 50-64, and just 15% of those 65 and older [1].

This pattern holds across most P2P platforms. Adults under 50 have adopted these tools at higher rates across the board [1]. For merchants with younger customer bases, P2P acceptance is essentially mandatory. For those serving older demographics, traditional payment methods remain important while P2P serves as a growing supplement.

Gen Z vs Baby Boomers: A 43-Point Gap

The Federal Reserve Bank of Atlanta’s 2024 analysis reveals the full extent of the generational divide. Their research found that 93% of Generation Z consumers (under age 25) have adopted mobile payment apps, compared to just 50% of baby boomers and older generations (65+) [2].

Even after controlling for income, education, and other demographic factors, the age effect persists. The Federal Reserve found that consumers under 25 were 33 percentage points more likely to have adopted a mobile payment app than those 65 and older [2]. This suggests the gap is not simply about income or technology access – it reflects genuine differences in payment preferences across generations.

Why Younger Consumers Prefer P2P Apps

The reasons for using P2P apps vary significantly by age. According to Pew Research, 44% of adults ages 18-29 who use these apps cite splitting expenses with others as a major reason, compared with 23% of those ages 30-49 and less than 10% of those 50 and older [1].

Users under 50 are also more likely to say that other people they know use these apps – indicating strong network effects that reinforce adoption among younger demographics [1]. For merchants, this means that accepting P2P payments can create a multiplier effect: customers who pay via Venmo or Cash App may encourage their friends to do the same.

Why Older Americans Resist P2P Adoption

Distrust is the primary barrier for older Americans. Two-thirds (67%) of Americans age 50 and older who have never used P2P apps say a major reason is that they do not trust these platforms with their money [1]. That share drops to 39% among those 18-49.

For merchants serving older demographics, this trust gap has practical implications. These customers may prefer traditional payment methods not because they cannot use P2P apps, but because they actively choose not to. Forcing P2P-only payment options could alienate this customer segment.

Cash App Demographics: Income and Race Patterns

Cash App shows distinct demographic patterns beyond age. According to Pew Research, 59% of Black Americans report using Cash App, compared with 37% of Hispanic Americans and smaller shares of White (17%) or Asian Americans (16%) [1].

Income also matters for Cash App specifically. Lower-income adults are most likely to use the platform: 36% of lower-income adults use Cash App, compared with 24% of middle-income and 18% of upper-income adults [1]. For merchants in communities with these demographics, Cash App acceptance may be particularly important.

| Platform | % of U.S. Adults Who Have Used |

| PayPal | 57% |

| Venmo | 38% |

| Zelle | 36% |

| Cash App | 26% |

Source: Pew Research Center, September 2022 [1]

Mobile Payment Adoption Continues Growing

The Federal Reserve Bank of Atlanta’s Survey of Consumer Payment Choice found that 72% of consumers had adopted online or mobile payment accounts (including PayPal, Zelle, Venmo, and Cash App) by 2023 – a statistically significant increase from 2022 [3].

As of October 2023, 70% of U.S. consumers had made a mobile payment at least once in the prior 12 months [2]. This broad adoption means that P2P payment acceptance is transitioning from a competitive differentiator to a baseline expectation for many customer segments.

Implications for Merchants

The data points to clear strategic implications. For merchants with customer bases skewing under 50, P2P payment acceptance is effectively mandatory – the vast majority of these customers have adopted the technology and many prefer it. For merchants serving older demographics, traditional payment methods remain essential, though P2P options can capture the growing minority who have adopted.

Cash App acceptance deserves special consideration for merchants serving lower-income communities or communities with large Black and Hispanic populations, where adoption rates are substantially higher than average [1]. Ignoring these patterns means losing sales to competitors who make payment easier for these customer segments.

Conclusion

The P2P payment landscape shows clear generational patterns. With 93% of Gen Z and just 50% of baby boomers adopting mobile payment apps, age remains the strongest predictor of P2P usage [2]. Platform preferences also vary: PayPal leads overall, but Venmo dominates among younger users while Cash App shows strong adoption among specific demographic groups [1].

For merchants, these patterns should directly inform payment acceptance strategy. Match your P2P offerings to your customer demographics, and you remove friction that costs sales. The data from Pew Research and the Federal Reserve makes one thing clear: P2P payments are no longer optional for businesses serving younger Americans.

References

- Pew Research Center – Payment apps like Venmo and Cash App bring convenience and security concerns to some users (September 2022)

- Federal Reserve Bank of Atlanta – Mobile Payments and the Exuberance of Youth (August 2024)

- Federal Reserve Bank of Atlanta – 2023 Survey and Diary of Consumer Payment Choice