How to Build Good Habits & Break Bad Ones (Data-Backed Guide)

Every year, millions of Americans set goals to save more money, exercise regularly, eat healthier, or break bad habits. Yet the data tells a sobering story about our collective struggle with behavior change. According to the Federal Reserve, the U.S. personal savings rate dropped to just 4.7% in late 2024 – down from a pandemic peak of over 30% – revealing how quickly financial habits can erode when external pressures ease [1].

The science of habit formation has advanced significantly in recent years. Research from University College London shows the popular 21-day rule is a myth – habits actually take an average of 66 days to form, with a range spanning 18 to 254 days depending on the behavior [2]. This article examines the data behind our habits and presents evidence-based strategies for lasting change.

The Data Behind Our Spending Habits

Consumer behavior data reveals clear patterns in how Americans allocate their money. According to the Bureau of Labor Statistics Consumer Expenditure Survey, the average U.S. household spent $77,280 in 2023 – up from $72,973 in 2022 [3]. Housing dominates at over $24,000 annually, followed by transportation and food.

These spending patterns reflect deeply ingrained habits. The categories where we overspend – dining out, entertainment subscriptions, impulse purchases – often happen on autopilot. Understanding that roughly 43% of daily behaviors are habitual helps explain why budgets fail: we’re fighting automatic processes with conscious willpower.

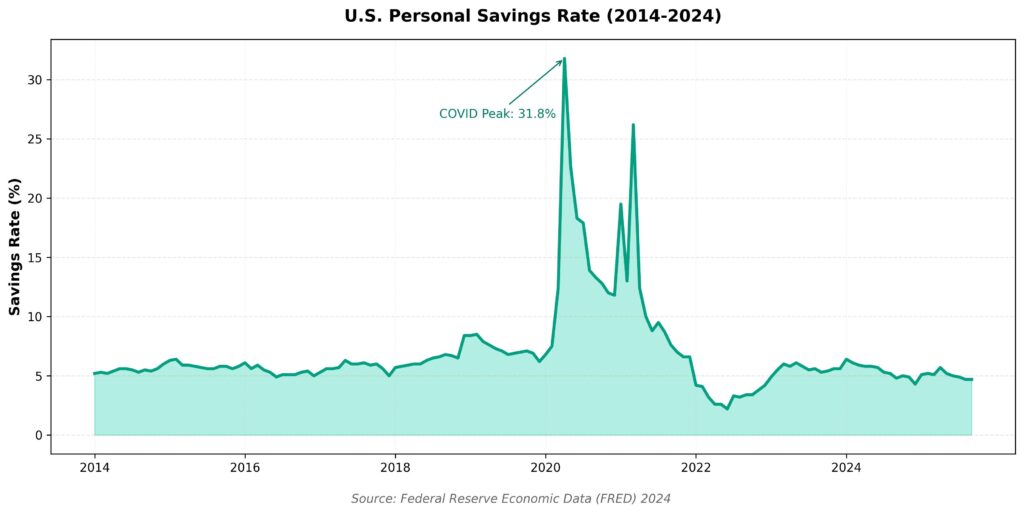

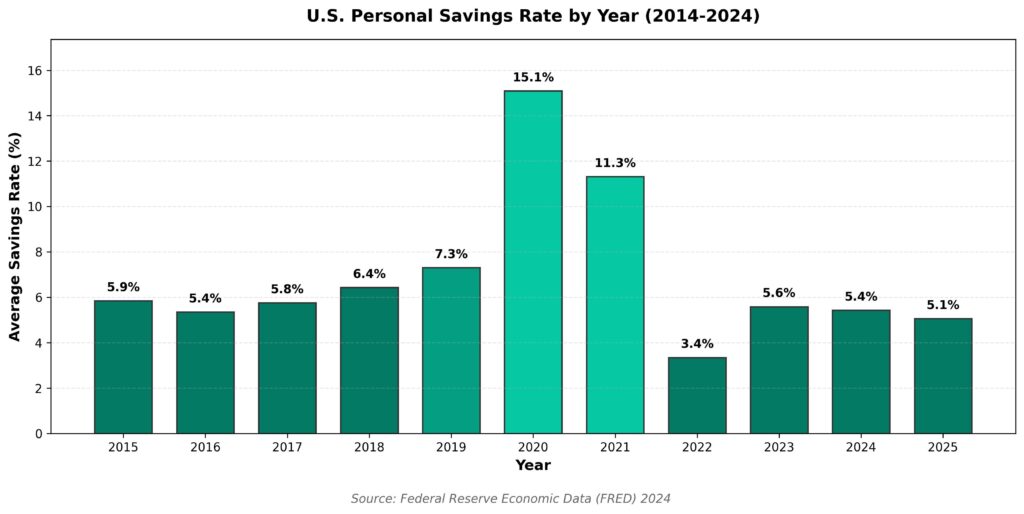

The Savings Habit: A Decade of Data

The personal savings rate offers a window into America’s financial habits over time. Federal Reserve data shows dramatic swings over the past decade, with the most striking shift occurring during the COVID-19 pandemic.

The pandemic created an unintentional savings experiment. With spending options limited and stimulus checks arriving, Americans saved at historic rates – peaking above 30% in April 2020. But as restrictions lifted, old spending habits returned almost immediately. By 2024, the savings rate had fallen back to pre-pandemic levels around 4-5% [1].

This pattern illustrates a crucial insight about habits: environmental changes can temporarily override behavior, but without deliberate habit-building, old patterns reassert themselves. The Americans who maintained higher savings rates post-pandemic were likely those who consciously automated their savings during the disruption.

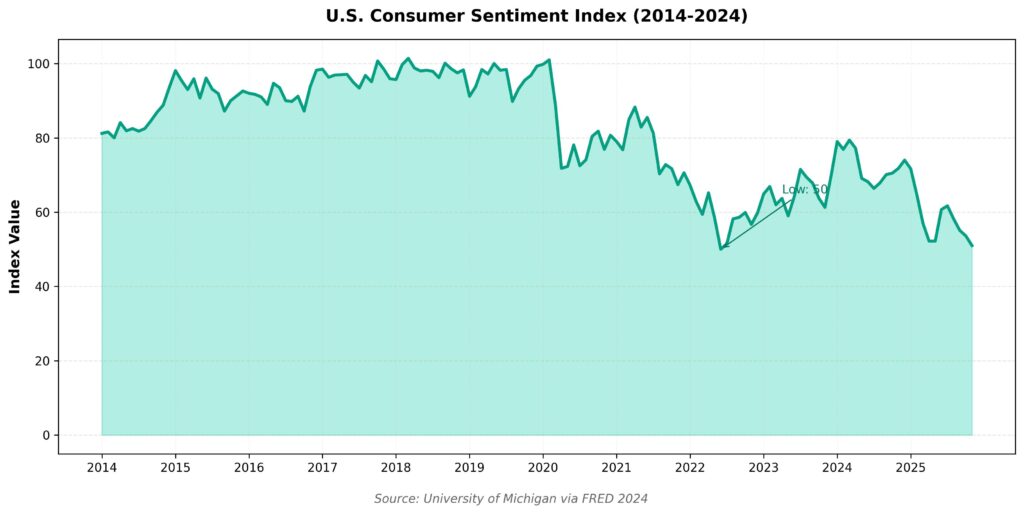

The Psychology of Habit Change

Consumer sentiment – a measure of how optimistic people feel about the economy – correlates with spending and saving behaviors. The University of Michigan Consumer Sentiment Index has tracked American attitudes since the 1960s, providing insight into the psychological drivers of financial habits.

The sentiment index hit historic lows in 2022 as inflation surged, yet consumer spending remained robust. This disconnect highlights an important truth about habits: they persist regardless of our conscious feelings. Even when people report feeling pessimistic about the economy, their habitual spending patterns continue largely unchanged.

Understanding the Habit Loop

MIT researchers discovered the neurological foundation of every habit in the 1990s: a three-part loop consisting of cue, routine, and reward. When you feel stressed (cue), you might scroll social media (routine), which provides temporary distraction (reward). Your brain releases dopamine during the reward phase, strengthening the neural connection [4].

Johns Hopkins University research shows that when you encounter cues associated with past rewards, your brain releases dopamine automatically – even when you’re not consciously thinking about the reward. This explains why breaking bad habits through willpower alone rarely works: the neurological response happens before conscious thought.

| Habit | Cue | Routine | Reward |

| Overspending | Stress/boredom | Online shopping | Dopamine rush |

| Saving | Payday | Auto-transfer | Security feeling |

| Exercise | Morning alarm | Gym workout | Endorphins |

| Snacking | TV time | Eat chips | Taste pleasure |

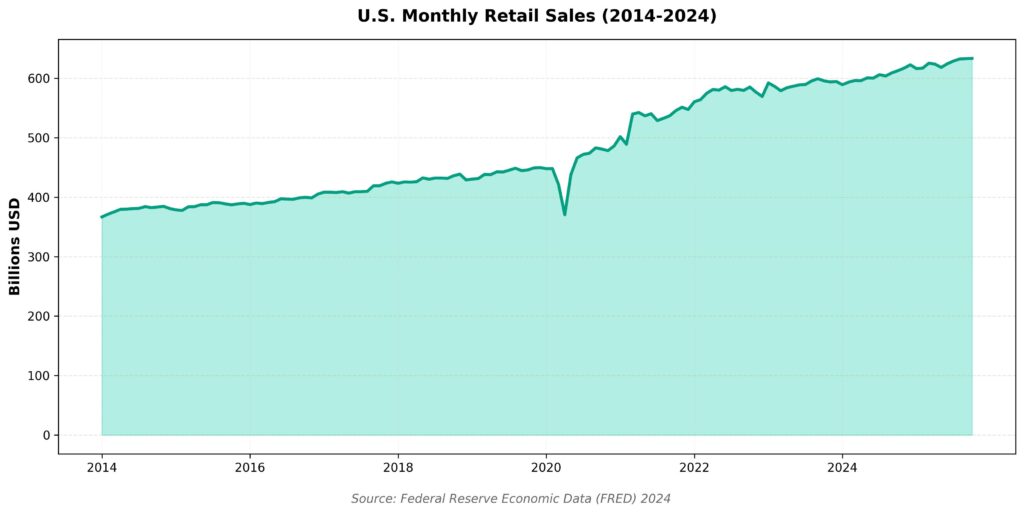

Retail Spending: Habits in Action

Monthly retail sales data shows how American spending habits have evolved over the past decade. Total retail sales (excluding food services) have grown from around $400 billion monthly in 2014 to over $600 billion in 2024 [1].

The steady upward trend reflects both inflation and genuine increases in consumption. E-commerce has been a major driver, growing from about 6% of retail sales in 2014 to over 15% today. This shift represents a fundamental change in shopping habits – one that happened gradually through the accumulation of small behavioral changes.

Proven Strategy #1: Automate Everything

The most effective habit strategy is removing decision-making entirely. Automated savings transfers, automatic bill payments, and subscription services for necessities eliminate the need for daily willpower. Research shows that people who automate their savings save significantly more than those who rely on manual transfers.

Set up automatic transfers to savings on payday – before you see the money in your checking account. This leverages the ‘pay yourself first’ principle and bypasses the mental negotiation that happens when you try to save what’s left over.

Proven Strategy #2: Start Ridiculously Small

The biggest mistake in habit formation is starting too big. Committing to save $500/month when you’ve never saved consistently sets you up for failure. Instead, start with a ‘minimum viable habit’ – $25/month, or even $5.

The 2024 research on habit formation confirms this approach: simpler behaviors like drinking water in the morning (median 59 days to automate) form faster than complex ones like regular exercise (median 91 days) [2]. Start small, establish the neural pathway, then scale up.

Proven Strategy #3: Habit Stacking

Habit stacking links new behaviors to existing automatic routines. The formula: ‘After I [current habit], I will [new habit].’ Research shows this approach increases habit adoption by 64% compared to starting habits in isolation [5].

Examples that work:

– After I pour my morning coffee, I will check my spending from yesterday

– After I receive my paycheck notification, I will transfer 10% to savings

– After I finish dinner, I will review tomorrow’s meal plan

– After I brush my teeth, I will do 5 minutes of stretching

Proven Strategy #4: Environment Design

Your environment shapes behavior more than intentions. To build good financial habits, remove friction from saving and add friction to spending:

For saving: Keep savings account separate from checking. Use apps that round up purchases and save the difference. Set savings account as default for direct deposit splits.

For spending less: Delete shopping apps from your phone. Remove saved credit cards from websites. Implement a 24-hour waiting period for non-essential purchases over $50.

Breaking Bad Financial Habits

Suppressing bad habits through willpower rarely succeeds long-term. The more effective approach is substitution: keep the cue, replace the routine with something that provides a similar reward.

If you stress-shop online, recognize the trigger (stress) and substitute a different routine that provides similar relief – perhaps a 10-minute walk or calling a friend. The key is finding a replacement that delivers some version of the reward your brain expects.

Common substitutions:

– Impulse Amazon shopping → Add to wishlist, review in 7 days

– Eating out when tired → Keep frozen meals stocked

– Subscription creep → Quarterly subscription audit

– ATM withdrawals for cash spending → Use a spending tracker app

The Power of Tracking

One-third of people who fail at new habits cite not tracking progress as the primary reason. Research shows that tracking doubles the likelihood of success. When you measure behavior, you create awareness; awareness enables adjustment [2].

For financial habits, tracking options include:

– Budgeting apps (YNAB, Mint, Copilot) that categorize spending automatically

– Weekly spending reviews – 10 minutes every Sunday

– Net worth tracking monthly

– The ‘don’t break the chain’ method for daily habits

Conclusion

The data is clear: Americans struggle with consistent habit formation, whether it’s maintaining savings rates, controlling spending, or building healthy routines. But the research is equally clear about solutions. Habits take 2-5 months to form, not 21 days. Automation beats willpower. Small starts beat ambitious failures. Environment design beats intention.

Start with one small, automated habit today. In three months, you’ll have a new baseline behavior. In a year, you’ll have fundamentally changed your financial trajectory. The compound effect of good habits is just as powerful as compound interest – and just as dependent on starting now.